Your Employees Are Financially Stressed: A Growing Benefits Trend Can Help Your Workforce (and Your Business)

Insights

4.02.25

Financial wellness programs are becoming one of the most in-demand employee benefits and are the focus of this year’s National Employee Benefits Day. Employers can use April 2 as a day to evaluate the effectiveness of their benefits packages amid a growing call for more flexible, personalized offerings from a workforce that is both rapidly evolving and financially stressed. Here’s how financial health benefits can help your employees – and your business.

National Employee Benefits Day 2025: A Focus on Financial Wellness Programs

National Employee Benefits Day, which falls on April 2 this year, was established by the International Foundation of Employee Benefits Plans (IFEBP) – an educational organization that serves plan sponsors and employee benefits communities in the U.S. and Canada. The day is recognized by employers, human resources professionals, benefits administrators, insurance providers, and other industry professionals – and this year the IFEBP is encouraging employers to focus on the financial wellness of their employees.

- Financial wellness and planning benefits include “any benefit that would provide knowledge or relief in money-related areas, such as retirement funds or budget counseling,” according to this article from the U.S. Chamber of Commerce. It cites nine benefits – including retirement plans, financial education and coaching, emergency fund access, student loan assistance, disability and life insurance, education costs, work-related stipends and reimbursements, personal financial assistance, and flexible paydays – as top examples.

- The IFEBP is calling on employers to evaluate whether they need to adjust their financial wellness programs to better serve their current employee populations: “Many employers and plan sponsors already make worker financial well-being a priority, but it may be time to take fresh look at these programs to ensure that they address emerging needs. What role could AI and other new tools play in financial education? How can programs be designed to address the unique needs of low-income workers or employee caregivers?”

A Snapshot of Today’s Multigenerational Workforce and Economic Environment

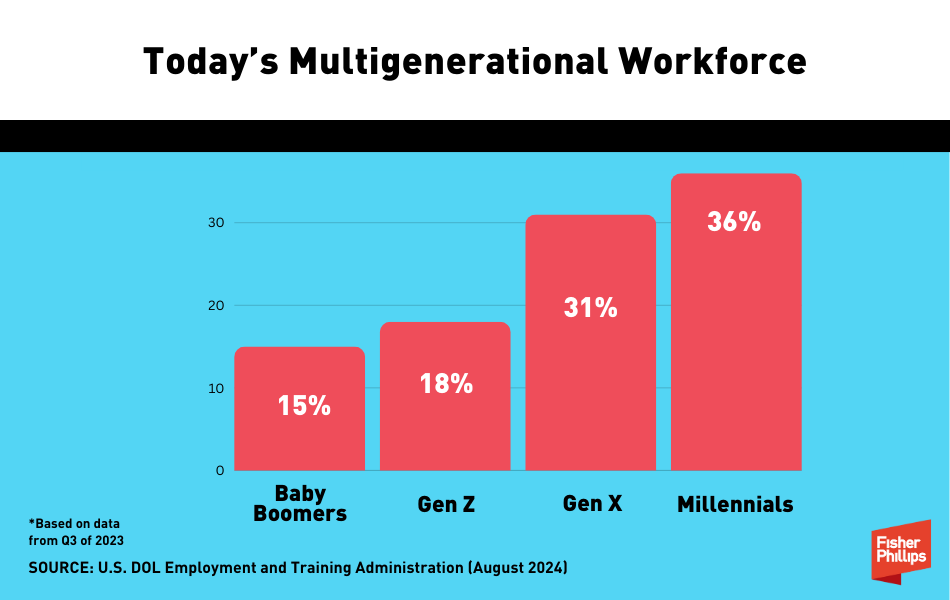

According to data from the U.S. Department of Labor, Gen Z surpassed Baby Boomers in the workforce for the first time in 2023. By mid-2024, the labor force by generations consisted of:

- 15% Baby Boomers

- 18% Gen Z

- 31% Gen X

- 36% Millennials

The Hartford’s 2024 Future of Benefits Report cited this wide range of generations as one of the key factors that employers should consider when designing a robust and rewarding benefits menu for their employees. “Layering on top of these generational challenges is a strained macroeconomic environment, including rising costs of living, that has caused many U.S. workers to feel financial stress,” according to the report. “This has prompted the need for more personalized benefits – and benefits-related education – to address financial security.”

Surveys Show Financial Stress Is Impacting Employee Productivity

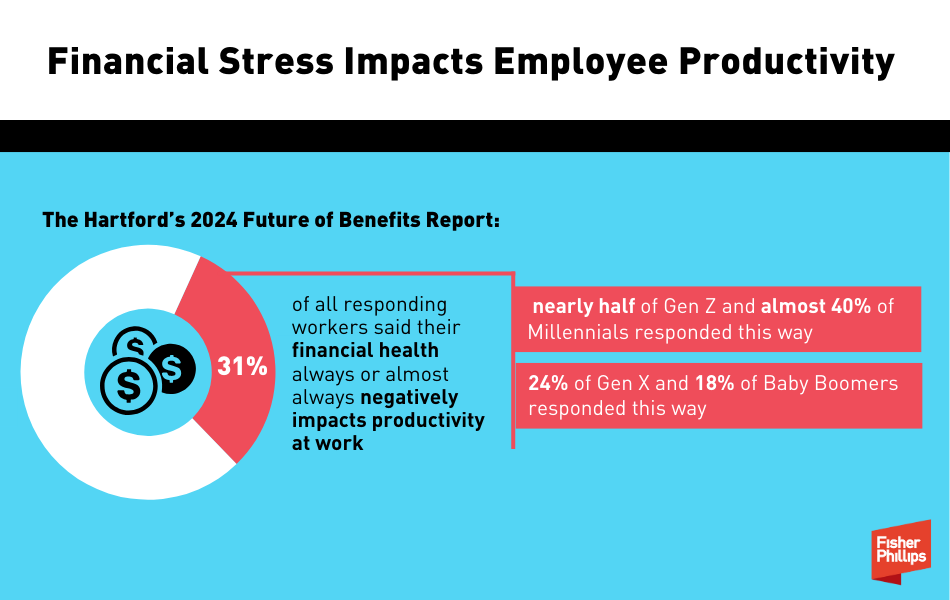

The Hartford’s report (linked above) includes results from a 2024 survey of more than 1,200 U.S. workers among roughly 500 employers. The results show that:

- 31% of all workers said their financial health always or almost always negatively impacts their productivity at work.

- Nearly half of Gen Z and almost 40% of Millennials responded this way.

- The share of the two preceding generations who also shared this sentiment was not insignificant – 24% of Gen X and 18% of Baby Boomers.

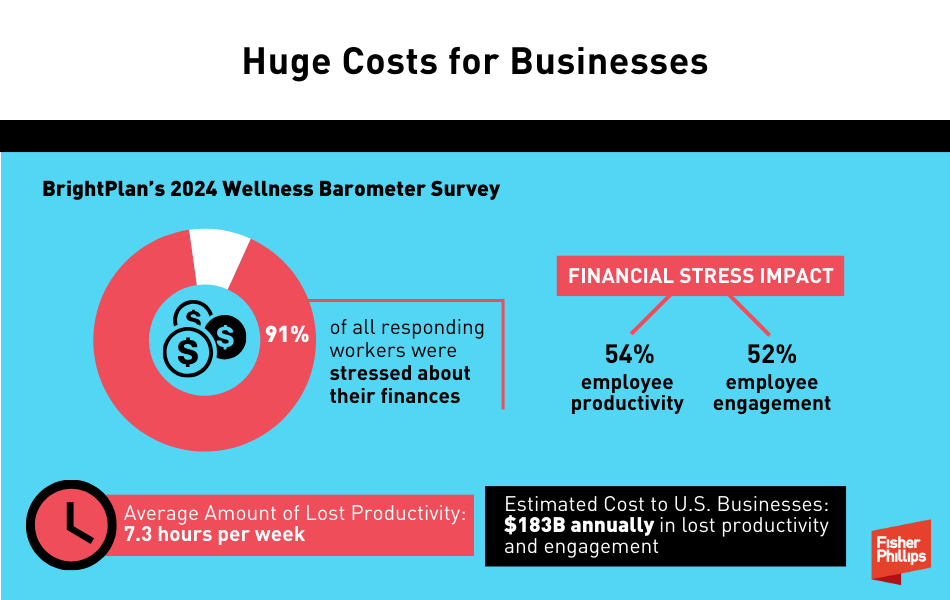

Results from another employee survey last year might be even more eye-opening. BrightPlan, an SEC-registered investment adviser that offers digital and human investment advice to U.S. residents, conducted a survey of 1,400 U.S.-based knowledge workers at global organizations with 1,000 or more employees. The survey found that:

- 91% of workers were stressed about their finances;

- financial stress impacted most workers in terms of employee productivity (54%) and engagement (52%); and

- “on average, each respondent is losing 3 hours of hours of productivity each week due to financial stress, costing U.S. businesses potentially $183B annually in lost productivity and engagement.”

BrightPlan’s report also showed a major gap between how leaders perceived their employees’ financial situations versus how employees would describe them.

|

Economic Conditions in 2025. The portion of workers impacted by financial stress could continue to climb this year, due in part to fears that the U.S. will enter a recession by year-end. In fact, a recent CNBC survey shows that 60% of the chief financial officers who responded said that they expect a recession in the second half of 2025, with another 15% projecting that a recession will hit soon – just not until next year. You can click here (FP Insight published in 2022) for general tips for employers to prepare for sustained economic volatility and ease workers’ inflationary concerns. |

How Employers Can Help: What to Consider and How to Get Started

Regardless of how long the current state of economic uncertainty lasts or what kind of impact it may have, financial wellness benefits remain a vital part of any competitive benefits package for today’s workforce. If you would like to improve your employees’ financial health – and their productivity on the job – here are some of the key points you’ll need to consider to get started.

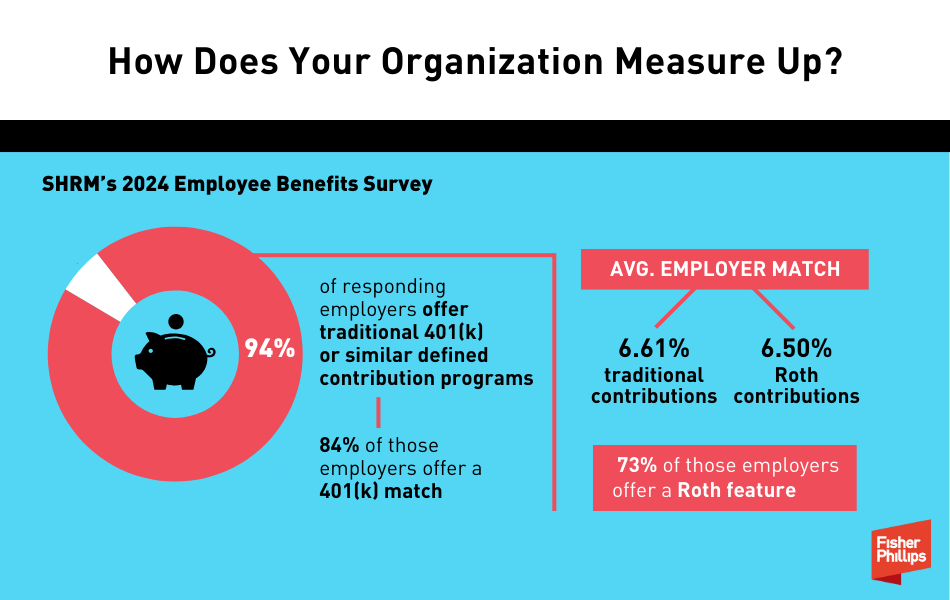

How does your organization measure up?

According to this SHRM report, which summarizes results from a 2024 survey of more than 4,000 U.S.-based professional members:

- 94% of employers offer traditional 401(k) or similar defined contribution programs;

- 84% of those employers offer a 401(k) match, with an average employer match of 6.61% for traditional contributions and 6.50% for Roth contributions; and

- 73% of those employers offer a Roth feature – up two percentage points from 2023 and up 10 percentage points from 2020.

Does your retirement plan permit pre-tax contributions up to the current IRS maximums?

Click here to learn more about the 2025 IRS limits for retirement plans and other benefits.

Are you up to speed on new plan requirements and options under the SECURE 2.0 Act?

The SECURE 2.0 Act, which President Biden signed into law in 2022, provides more flexibility to employer-sponsored qualified retirement plans, including by permitting new features such as emergency distributions, emergency savings accounts, and matching contributions for student loan payments. These optional plan features could be particularly valuable for employees this year due to the uncertainties related to the economy and federal student loan programs.

| Mounting Student Loan Problems. As federal loan borrowers ride out the rollercoaster of pandemic payment pauses, legal challenges to the Biden administrations forgiveness plans, court actions impacting income-driven repayment plans, and President Trump’s recent executive order attempting to shut down the Department of Education entirely, it should come as no surprise that federal student loan delinquency rates have reached a record high. The Federal Reserve Bank of New York recently estimated that 9 million borrowers “will face significant drops in credit score once delinquencies appear on credit reports in the first half of 2025.” For more on helping your workers struggling with student debt repayment, click here. |

The SECURE 2.0 Act also added new requirements that could help improve your employees’ financial health, such as mandatory automatic enrollment for certain retirement plans. The federal law has been rolling out over time, and some of its provisions took effect just this year. You can read all about it here and here. Work with benefits counsel to determine whether your plan requires any changes for compliance purposes or to add new permissible features (if you opt to do so) that could enhance your financial wellness offerings.

Do your employees understand how to participate in and benefit from your retirement plan?

By increasing your efforts to educate employees about the retirement benefits you offer, you could potentially increase how many eligible employees participate in (and how much they contribute to) your plan – improving employee financial wellness through existing benefits.

Do you offer employees any nonretirement financial advice benefits?

The SHRM report flagged nonretirement financial advice as one of the “benefits to watch” – noting a slight uptick last year in offering nonretirement financial advice benefits (32%) and credit counseling services (16%).

These benefits might include access to financial education through an employee assistance program, artificial intelligence tools (and, eventually, AI agents), and in-person classes and coaching led by finance professionals. Many new tools can be personalized to fit the individual needs of your employees, regardless of their income levels and other differentiating factors.

What types of family care benefits do you offer?

The U.S. is facing crises in both child care and elder care, and the surging costs of both (not to mention the growing demand for unpaid caregiving) is crippling many Americans.

For deeper dives on supporting the parents in your workforce, as well as your employees managing both child and elder care, check out these prior FP Insights:

- Olympic Moms Are Changing the Game and So Can You: 5 Ways Employers Can Support the Olympic Feat of Balancing Work and Family

- 5 Ways to Support Employees in the Sandwich Generation Managing Child and Elder Care

In the meantime, here are a few quick points on family care benefits:

- Child Care. A recent report shows that childcare is more expensive than public college tuition in 38 states and Washington D.C. – as high as $2,363 per month for a household with one infant. As for good news, the SHRM report shows a significant increase in worksite lactation/mother’s rooms in 2024 (likely due to a federal law enacted in 2022), which could potentially improve women’s financial health by enabling them to not only return to work but also choose whether to breastfeed or formula feed, which can be cost-prohibitive. However, SHRM states that “other on-site offerings for child care have not kept pace,” and that “child care center benefit offerings, already at very low prevalence rates, have been cut in half since 2021, whether subsidized (3%) or unsubsidized (2%).”

- Elder Care. “Much of the recent emphasis on paid leave has focused on new parents, which is important,” the SHRM report notes. “However, with 14% of the U.S. population providing unpaid elder care, employers might also consider the risks to their current and future talent needs by failing to offer benefits to help their workforce manage elder care concerns, which will only increase.” But the report shows a slight decrease last year in employers that offer elder care referral services (13%) or elder care subsidies (1%) – making this a key area for improvement. You might also consider offering voluntary long-term care insurance benefits to help your employees plan for their own future long-term care costs, should they ever arise.

- Pet Care. While laws haven’t yet mandated pet care leave (though NYC recently considered it), an increasing number of employers (22% in 2024, per the SHRM report) are offering pet health insurance to help offset veterinary care costs. SHRM notes that “American households are now more likely to have pets than children under 18,” and pet insurance “can be a relatively low-cost, low effort benefit for employers to provide.”

Conclusion

We will continue to provide tips, guidance, and updates on employee benefits and other workplace law topics, so make sure you are subscribed to Fisher Phillips’ Insight System to get the most up-to-date information directly to your inbox. If you have questions, feel free to reach out to your Fisher Phillips attorney, the author of this Insight, or any attorney in our Employee Benefits and Tax Practice Group.

Related People

-

- Jennifer S. Kiesewetter

- Partner